Shauna joined the BD team at Integrum ESG in 2021, having previously worked in similar roles within Fintech companies. She holds a BA in English and New Media Studies from the University of Limerick, Ireland.

Controversial activities is the ESG term for the categories of business activity that asset managers, asset owners, regulators and ratings providers commonly want to exclude or monitor at the portfolio level.

Categories includes tobacco, alcohol, gambling, fossil fuels, weapons and defence, civilian firearms, palm oil, prisons and law enforcement, animal products and others. Controversial weapons sits inside it as a narrower sub-set, but many exclusion mandates today reach further than weapons alone.

The list of activities considered controversial is not formally codified in any single regulatory document. It has emerged from a combination of EU Sustainable Finance Disclosure Regulation (SFDR), EU Climate Transition Benchmark (CTB) and Paris-Aligned Benchmark (PAB) exclusions, ESMA fund naming guidelines, MiFID II client suitability rules and decades of asset owner mandate criteria.

This article looks at the categories most commonly treated as controversial, the regulatory and mandate drivers behind their growing importance, the gaps in the data currently available to investment teams, and how Integrum has built its Controversial Activities dataset to address them.

Across ESG data providers and regulatory frameworks, the following activity categories are most commonly treated as controversial:

Each parent category contains sub-groups that capture different parts of the value chain.

Tobacco, for example, breaks into cigarette manufacturers, the tobacco supply chain and vape and e-cigarette producers.

Weapons and Defense includes military weapons, military software and IT services, military infrastructure and military other services as distinct sub-categories.

Exclusion-based screening is one of the most widely adopted responsible investment approaches in the market. The PRI's introductory guide to screening and exclusions estimates that around $3.8 trillion in assets are subject to negative or exclusionary screens, with another $1.8 trillion under norms-based screens. Three forces have driven this further into the mainstream over the last three years.

Regulatory requirements

SFDR Article 8 and 9 funds must report on a set of Principal Adverse Impact (PAI) indicators, including exposure to controversial weapons and exposure to the fossil fuel sector. EU CTB and PAB regulations additionally require exclusions for controversial weapons, tobacco production and significant fossil fuel involvement.

ESMA's fund naming guidelines apply CTB or PAB exclusions to funds using ESG, sustainable, transition or Paris-aligned in their names. The evolving SFDR 2.0 framework is expected to extend rather than relax these requirements, with tobacco and controversial weapons proposed as binary exclusions across all categorised products.

Client mandates

Asset owners, faith-based investors, wealth management clients and SRI funds increasingly specify which activities are excluded at the portfolio level. Catholic exclusions, Islamic finance screening and bespoke ethical mandates often go further than regulatory minima and require granular, defendable data on every holding.

Reputational and operational risk

Holdings that appear on a controversial activities list create reputational exposure for fund managers, retail wealth platforms and pension trustees. Pre-trade compliance and ongoing portfolio monitoring on these exposures are now standard practice across most institutional firms.

Three problems define how investment teams have historically worked with this data.

Fragmentation across products

Most providers split this data into multiple products. MSCI sells Business Involvement Screening Research, Sustainable Impact Metrics and SDG Net Alignment Score. Sustainalytics sells Product Involvement, Sustainable Products Research and the EU Taxonomy Solution. Clarity AI and ISS ESG follow the same pattern. Each requires its own implementation, its own subscription and its own data feed.

Imprecise revenue exposure

Several providers publish revenue exposure in ranges rather than specific percentages, for example 0-4.9%, 5-9.9% and 10-24.9%. For asset managers needing to apply explicit revenue thresholds to portfolio construction or mandate monitoring, ranges are difficult to work with operationally.

Limited transparency on methodology

Companies frequently do not disclose the proportion of revenue derived from controversial activities. To produce specific percentages, providers must either estimate or model the data. Most do. Few show the workings.

These gaps matter when investment teams need to defend exclusion decisions to clients, trustees or regulators.

Controversial activities data supports several distinct use cases across an investment business:

1. Portfolio construction

Exclusionary, best-in-class and thematic portfolios built from a screened starting universe, with every screen traceable to source.

2. Mandate fulfilment

Institutional, faith-based, ethical and individual wealth client mandates run against one audited source. Catholic exclusions, Islamic finance, SRI and bespoke retail client requirements are all supported from the same dataset.

3. Regulatory disclosure

SFDR Article 8 and 9 product classification, SFDR PAI reporting, ESMA fund naming compliance, MiFID II client suitability and the FCA's SDR labels.

4. Risk management

Pre-trade compliance, ongoing portfolio monitoring and reputational risk identification before exposure appears in the news.

5. Stewardship and engagement

Targeting engagement on companies with material revenue exposure to specific controversial activities, and tracking exposure shifts over time.

Integrum has launched Controversial Activities data to address these three gaps directly.

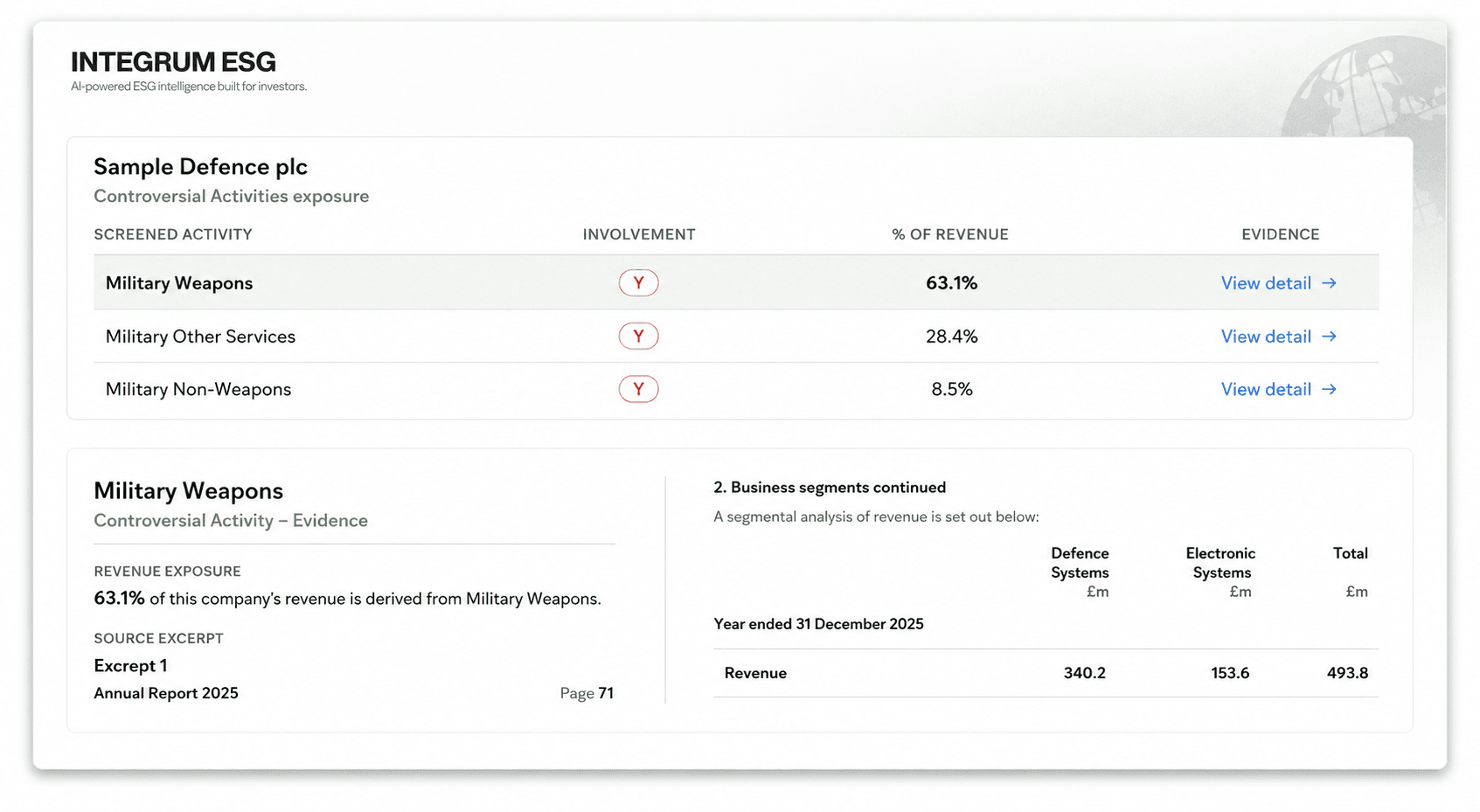

Exposure is calculated at the product-line level, not the company level. A diversified business is shown only on the parts that fall within scope. Specific revenue percentages are shown where audited filings disclose them. Where exposure is confirmed but the filing does not quantify it precisely enough, we flag it as Y. No estimates are passed off as confirmed numbers.

Each of the 14 controversial categories is defined by activity-level rules covering producers, suppliers, distributors, financiers, infrastructure providers and companies serving controversial end-markets. The criteria are not limited to pure-play producers, so a diversified company with partial exposure is captured rather than missed.

Every classification is built from 10-Ks, 20-Fs, 40-Fs, annual reports and sustainability reports. Not from third-party databases, not from estimates and not from self-reported scores.

Every percentage and every flag links directly to the relevant excerpt from the company's source filing, with page references. Investment teams can open the underlying disclosure, read the verbatim text and defend the number to clients, trustees or regulators.

Controversial Activities classifications connect to related revenue datasets across the Integrum platform, including UN SDG alignment, EU Taxonomy eligibility and standard industry classifications. A company classified once flows through every framework an investor reports against.

Most controversial activities data in the market was procured years ago, on multi-year terms, and has rarely been reviewed since. The criteria that mattered at the last renewal are rarely the criteria that matter now.

A few useful questions if you are scoping a change:

The honest way to find out is a side-by-side comparison on names you already screen. Share a handful of holdings and we will show you the data, the source citation and the evidence on the same screen.

Browse frequently asked questions about the platform.

Can’t find the answer you’re looking for? Please get in touch with our team.