Harish joined the Business Development team at Integrum ESG after having previously overseen BD for the investment network Venture Giants, and also worked within the Customer Experience Program Team at Amazon. He has a BSc in Philosophy, Logic and Scientific Method from the London School of Economics and Political Science.

The market for ESG ratings is concentrated around a small group of established providers, among them MSCI, Sustainalytics, S&P Global, ISS and LSEG/Refinitiv.

For the asset managers who buy them, the price of these ratings has held firm while the product behind it has not kept pace. The data behind these ratings is often months out of date, patchy across sectors and almost impossible to explain, yet the price has not moved to reflect that.

That gap between price and quality is worth examining, and there is a more efficient way to source the same data.

This article sets out what the legacy ratings providers actually charge for, why a lagging and limited product still commands a premium, and what to look for in an alternative, whether that means replacing an incumbent or running a second source alongside one.

When a manager subscribes to a legacy ESG rating provider, the licence fee is often only the start of cost accumulation:

None of this comes for free. To work around lagged data, coverage gaps and opaque methods, managers run multiple feeds, build their own internal overlays to normalise inputs across vendors and absorb many analyst hours spent cleaning and reconciling data before it can be used.

That effort is the hidden second cost of a legacy rating, and it is now quantified.

In its December 2025 consultation on bringing ESG ratings into supervision, the FCA estimated the market carries around £495m a year in costs, driven largely by the due diligence asset managers and pension schemes do to understand or verify ratings. Firms pay the incumbent for the rating, then pay again in time and effort to make it usable.

ESG can end up sidelined as a result, kept as a reporting formality or carried into risk decisions despite the gaps in the data.

The rest of this article looks at how the pricing reached this point, and at what a more current and transparent alternative looks like.

ESG ratings began as a low-cost tool, a simple way for institutions to satisfy compliance and marketing requirements. Demand rose sharply through the SFDR rollout, and the established providers priced into it.

Today the ratings are deeply embedded across the investment chain and are used in portfolio construction, reporting and stewardship.

That entrenchment is the point - because most firms hold ESG ratings to evidence a process to clients and regulators, quality historically was rarely the deciding factor at the point of purchase.

With quality doing little to discipline price, what a legacy provider charges reflects its market position and the budgets of its largest clients more than the accuracy or currency of the data. Product offerings from legacy providers have hardly changed, yet the price has increased year over year regardless.

The same dynamic explains why the price is not only high but inconsistent.

Two firms can be quoted very different amounts by the same provider for what is effectively the same package, because ESG ratings are sold through private, bilateral negotiation and are rarely benchmarked between buyers.

There is little reference point to push against, and when managers do benchmark, they often find they have been paying well above the market, in our experience around three times what the same coverage costs from a transparent provider.

As larger buyers absorbed premium pricing with little resistance, that level settled in as the market reference, and smaller firms have tended to match it rather than risk looking less rigorous than their peers.

These concerns, over both methodology and pricing, are now being directly addressed by international regulators.

IOSCO, the international body for securities regulators, has flagged opaque methodologies, uneven coverage and conflicts of interest among ESG ratings providers, including how their fees are structured and the sale of advisory services to the same issuers they rate.

EFAMA, the European fund managers' association, has raised the lack of transparency around both the methodologies and the pricing of the established providers.

Those concerns now sit at the centre of incoming regulatory changes.

The EU ESG Ratings Regulation applies from July 2026, after which only authorised providers will be able to operate in the EU, and they will have to publish their methodology and meet stronger governance requirements.

In the UK, the FCA is bringing ESG ratings into supervision for the first time, with final rules expected in late 2026 and the regime taking effect from 29 June 2028.

The FCA's own research found that around half of users are concerned about how ratings are built, with 55% worried about how they are developed and 48% about the transparency of methodologies and data. We recently examined the transparency gaps that remain even after MSCI's latest methodology change in our analysis of its Version 5 update, and the pattern across the legacy providers is consistent.

These limitations are not unique to any one name. Managers pay high and persistent prices for products whose construction and pricing they cannot fully see.

Integrum ESG was built as a direct response to the issues above, by a founding team that lived them.

Our founder and CEO Shai Hill worked in asset management, including a decade as Head of Research at Macquarie Group before founding Integrum in 2018, and built the product around the data he could not get from incumbent providers.

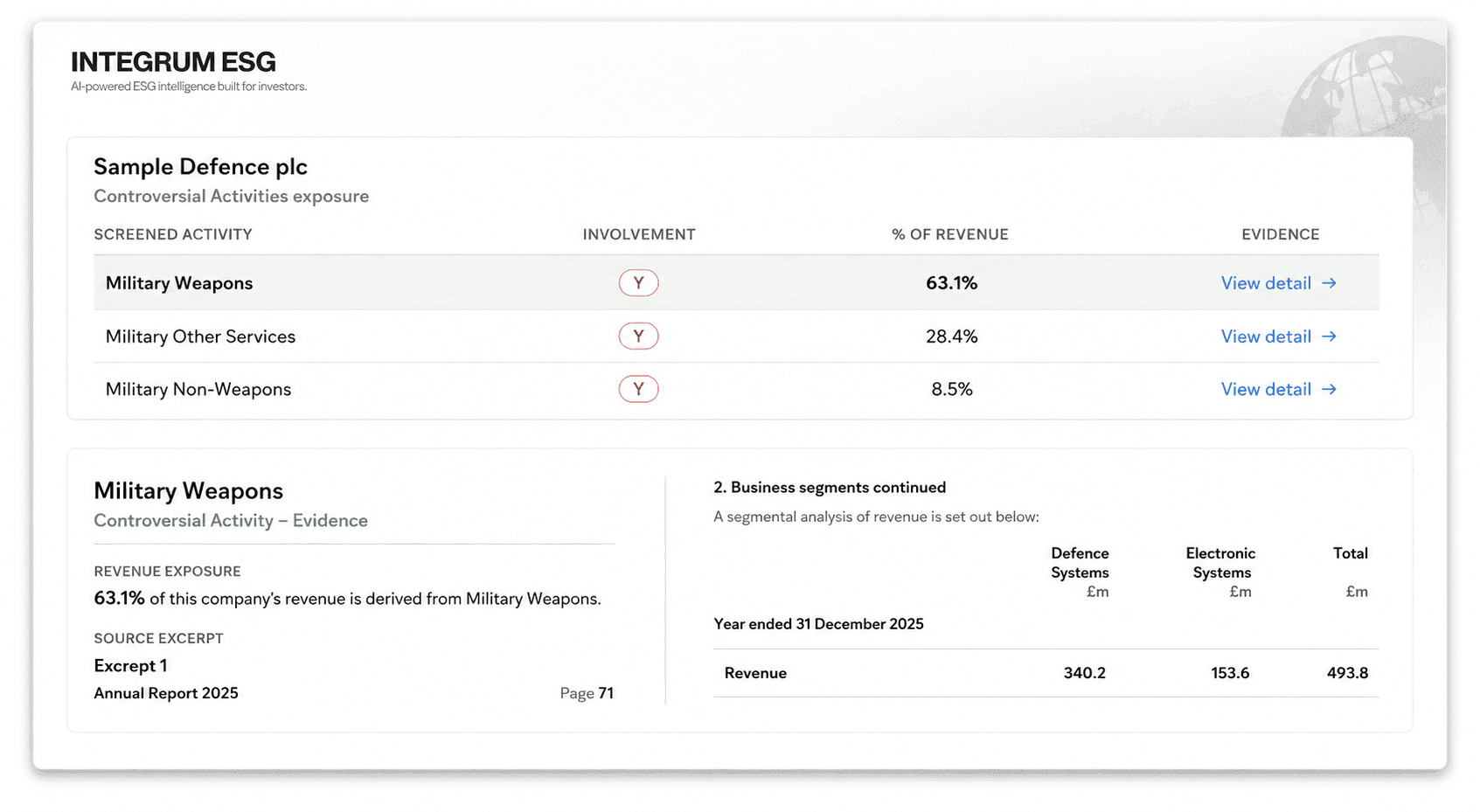

It is an alternative to the legacy ESG ratings providers, built on proprietary AI models with human-in-the-loop review, so disclosures are captured and structured quickly and then checked by ESG analysts before publication.

The result is data that is fully traceable, current and openly priced. Our Glass Box Data framework shows the full path from source disclosure through to scoring and final output, with every data point traceable to where it came from.

For asset managers, that means:

The intention is straightforward. Clients see exactly what they are paying for and avoid paying a premium for data they then have to repair.

Integrum's full solutions suite shows how this works across companies, funds, sovereigns and private markets.

You do not have to replace a legacy provider to benefit. Integrum ESG works both ways:

For many managers the simplest first step is to keep their current provider in place and run a side-by-side comparison via our complimentary overlap period. The difference in coverage, freshness and price becomes clear without disrupting existing workflows.

Renewal cycles, methodology changes and new regulation all tend to prompt a review of ESG data arrangements, and with the EU regime taking effect in July 2026 and the UK regime following in 2028, the question is moving into sharper focus.

If you are reviewing your ESG data this year, a few questions are worth asking:

The most useful first step is a direct comparison. Send us the package you currently pay for and we will show you the difference in coverage, freshness and price.

Browse frequently asked questions about the platform.

Can’t find the answer you’re looking for? Please get in touch with our team.