Harish joined the Business Development team at Integrum ESG after having previously overseen BD for the investment network Venture Giants, and also worked within the Customer Experience Program Team at Amazon. He has a BSc in Philosophy, Logic and Scientific Method from the London School of Economics and Political Science.

First reported on by Dominic Webb of Responsible Investor - original article can be found here.

A leaked European Commission draft suggests a sweeping redesign of the Sustainable Finance Disclosure Regulation (SFDR) - simplifying fund classifications, cutting back reporting burdens and redefining how sustainability information is presented to investors.

Alongside outlining the key changes, this article draws on perspectives from across the market - including fund managers, ESG consultants and sustainable finance specialists - to explore what the draft overhaul could mean in practice for investors and managers.

There are now three new proposed product categories, to replace the existing Article 6, 8 and 9 structure :

Must invest at least 70 percent in assets with measurable transition objectives such as taxonomy-eligible activities, companies with credible transition plans or science-based targets.

Simon Abrams, former Director of Sustainable Finance at EY and founder of consultancy Elpis Impact, welcomed this addition, highlighting its potential to channel capital toward meaningful change:

“I welcome the introduction of an Article 7 category. Most impact can be generated by transitioning underperforming environmental companies into high-performing ones.

If properly defined, this will give investors confidence to invest in brown-to-green impact, which was previously unclear.”

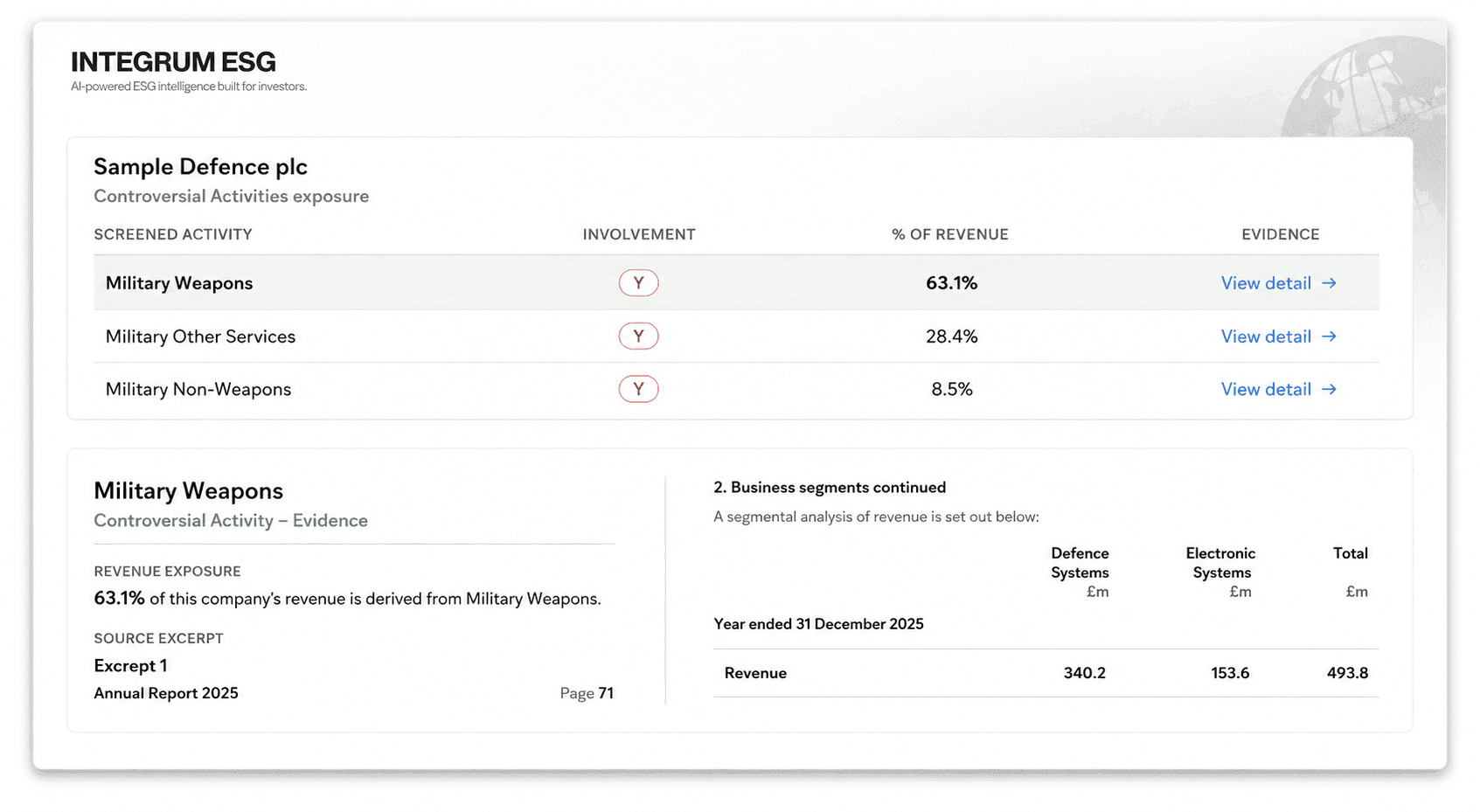

Abrams also noted that the new defence-related exclusions present a nuanced challenge:

“The defence exclusions are particularly interesting - it’s a more limited exclusion set than some existing fund policies. The EU has been clear that ESG rules shouldn’t hinder support for the defence sector, given EU NATO members commitment to spending at least 3.5% of GDP.

This will create challenges for defence value-chain companies to disclose fully, but also incentivises them to prioritise sustainability to attract finance.”

Cover products that integrate sustainability factors through metrics such as above-average ESG ratings or measurable outperformance on sustainability indicators.

While the new category aims to streamline how ESG factors are applied across mainstream strategies, some market observers warn that looser entry criteria could even widen the loopholes that allowed limited-ambition funds to qualify under the current regulation.

Must allocate at least 70 percent of assets to sustainable economic activities (down from 100 percent) including EU green bonds or Paris-aligned benchmark assets while excluding companies expanding fossil-fuel capacity or lacking coal phase-out plans.

Molly Frazer, Head of Research at Integrum ESG, said the lower allocation threshold brings opportunity - but also risk:

“The shift from 100% to 70% sustainable allocation expands the universe of Article 9 funds, but risks watering down the label.

Strong, enforceable criteria need to be set out in the Regulatory Technical Standards to ensure Article 9 reflects real sustainability outcomes, not just aspirations.”

Asset managers would no longer be required to publish firm-wide (entity-level) Principal Adverse Impact (PAI) statements.

The draft explicitly deletes Articles 4 and 5 of the SFDR, removing the current “comply-or-explain” regime for PAIs.

According to the Commission’s impact assessment, this would cut compliance costs by roughly €56 million per year, with entity-level sustainability disclosures instead expected to flow through the Corporate Sustainability Reporting Directive (CSRD).

The proposal also repeals Article 7 of the SFDR Adverse Impacts. These PAI templates and indicators would therefore disappear in their current form.

In their place, the new framework introduces simplified product-category disclosures (Transition, Integration and Sustainable funds) that include key sustainability metrics and exclusion lists, but no dedicated PAI statement. The Commission has been asked to draw up these new indicators and although they are expected to draw on the current PAIs, these will be voluntary.

The draft also clarifies that use of the new fund labels will be voluntary for alternative investment funds (AIFs) marketed exclusively to professional investors.

In practice, however, most managers are expected to retain the classifications given continued demand for transparency from limited partners and institutional allocators while new funds should continue to seek them to meet client expectations.

Joe Mares, Portfolio Manager at London based hedge fund Trium Capital, illustrates this pragmatic approach to the evolving disclosure landscape:

“Regulations on fund disclosure have changed before and will change again.

Our focus is on translating ESG data and energy-transition strategies into investment performance and measurable impact.

We’ll continue to disclose what’s required - and go further where it adds value for our investors.”

The draft introduces formalised rules for greater clarity on the use of estimates, requiring investors to explicitly disclose when and how they apply estimated data in fund reporting.

This move reflects the Commission’s wider focus on improving data reliability and auditability across sustainable finance regulation. Transparency on data quality has been a recurring demand from both regulators and allocators and will likely form a key test of reporting credibility under the revised framework.

The Commission plans to remove the formal definition of a “sustainable investment,” embedding sustainability criteria directly into the rules governing each product category.

While this may simplify implementation, it raises questions about how investors and regulators will determine consistency and comparability in the absence of a clear legal definition.

Without defined parameters, interpretations of what constitutes a sustainable investment may continue to vary across jurisdictions.

Shai Hill, Founder & CEO of Integrum ESG, cautioned that removing this core definition risks undermining consistency across the framework:

“Removing the definition of a sustainable investment raises a fundamental question of how regulatory challenges to fund names might be guided.

If legislation is designed to regulate sustainable investments, it must also define what they are and are not. A clear legal definition is essential for consistent interpretation and enforcement.”

The proposals, if adopted, would mark the most significant rewrite of SFDR since its launch.

For investors and managers, the proposals would reshape both reporting expectations and how sustainability claims are evidenced. Specific implications include:

While firm-wide PAI reporting will disappear, product-level disclosures will demand consistent, data-driven evidence of sustainability claims in line with their chosen product category.

The new emphasis on disclosing estimates strengthens the regulatory push for credible, verifiable data in sustainability reporting.

The move to the new three fund types is designed to help allocators understand which products drive transition, integrate ESG or target sustainability directly.

Mandated fossil-fuel and coal-phase-out exclusions create a de facto minimum standard for sustainable and transition-labelled funds.

Taken together, these changes reflect an effort to make SFDR more workable in practice while preserving its core objectives of transparency and comparability.

This is a direction that has been welcomed by industry observers such as Chessie Lindsay Brown, ESG Consultant at Danesmead Advisory, who commented:

“While the SFDR updates are unconfirmed, we're excited to see the next phase in the long-awaited SFDR 2.0 emerge.

It seems that the framework is moving forward with a practical repurposing of the existing Articles, which should help minimise confusion for market participants.

We welcome the elimination of entity level PAI reporting and the introduction of exclusions for labelled products, bringing SFDR more in line with other regulatory labels of this kind.”

Although the revised SFDR seeks to improve clarity through defined product categories, the loosened requirements could once again open space for misuse.

The absence of a precise legal definition of “sustainable investment” and the voluntary use of Principal Adverse Impact indicators grant managers broad discretion in how funds are labelled.

Article 8, for instance, illustrates how products with limited ESG ambition could still qualify as sustainable - a risk that mirrors many of SFDR’s current shortcomings.

Unless the forthcoming Regulatory Technical Standards introduce firmer minimum safeguards, there remains a material risk that these reforms could entrench, rather than reduce, greenwashing across the market.

The European Commission is expected to formally confirm the SFDR amendments on 19 November 2025.

Investors and the wider market will be watching closely for confirmation of these proposals and any further guidance on implementation timelines.

Abbie Main, Head of Business Development at Integrum ESG, noted that the challenge ahead may be less about compliance and more about communication:

“The streamlined categories should help with internal classification, but communicating these changes to clients will be a key challenge.

Many allocators still associate Article 8 and 9 with specific expectations, and shifting that narrative will require clear, consistent messaging from managers.”

Integrum ESG will continue to monitor developments and provide further analysis as the review progresses, and implementation details emerge.

Browse frequently asked questions about the platform.

Can’t find the answer you’re looking for? Please get in touch with our team.