Shrey joined the BD team at Integrum ESG in 2025, bringing corporate and institutional relationship management experience. She previously worked at HSBC, where she supported Global Financial Sponsors and Private Equity-backed companies on complex transactions and financial solutions. Shrey holds an MEng in Mechanical Engineering from the University of Bristol and an Advanced Diploma in Banking and Finance from LIBF.

A landmark new regulation regarding the global shipping sector was announced in April.

The International Maritime Organization (IMO) formally introduced a “carbon credit” regime, marking a significant shift in the industry’s approach to climate responsibility.

This is the first time a world-wide, sector-specific carbon pricing model has been established, designed to move shipping towards net-zero by 2050.

Regulatory scope and coverage

The new regulations will come into force from 2027, applying to all large marine vessels over 5,000 gross tonnage, which are responsible for 85-90% of international shipping’s CO₂ emissions.

The mechanism is designed to be universal: all 176 IMO member states are subject to the rules.

How does the proposed regime work?

The system introduces two levels of Scope 1 Greenhouse Gas (GHG) Emissions targets:

• Ships that exceed the base emissions threshold will pay a fee of $100 per tonne of CO₂ emitted above that level

• The most polluting ships, above a stricter threshold, will face a charge of $380 per tonne of CO₂

Ships that outperform targets can earn credits, which they can sell to others, creating a market incentive for early adopters of low- and zero-emission solutions.

What are the implications for investors?

The new IMO regulation directly impacts a company’s share price:

📉 Higher emissions = higher costs → lower profits and share price

🚀 Decarbonisation leaders gain better valuations and investor trust

⚠️ Carbon pricing widens the gap between leaders and laggards - investors must reassess portfolio risks and opportunities

With carbon priced in, ESG performance is now a key driver of market value.

In-scope companies worth investor attention

Using the Integrum Platform, we screened in-scope companies in the Marine Transportation industry, initially ranking them by scaled Scope 1 GHG emissions (Emissions / Revenue).

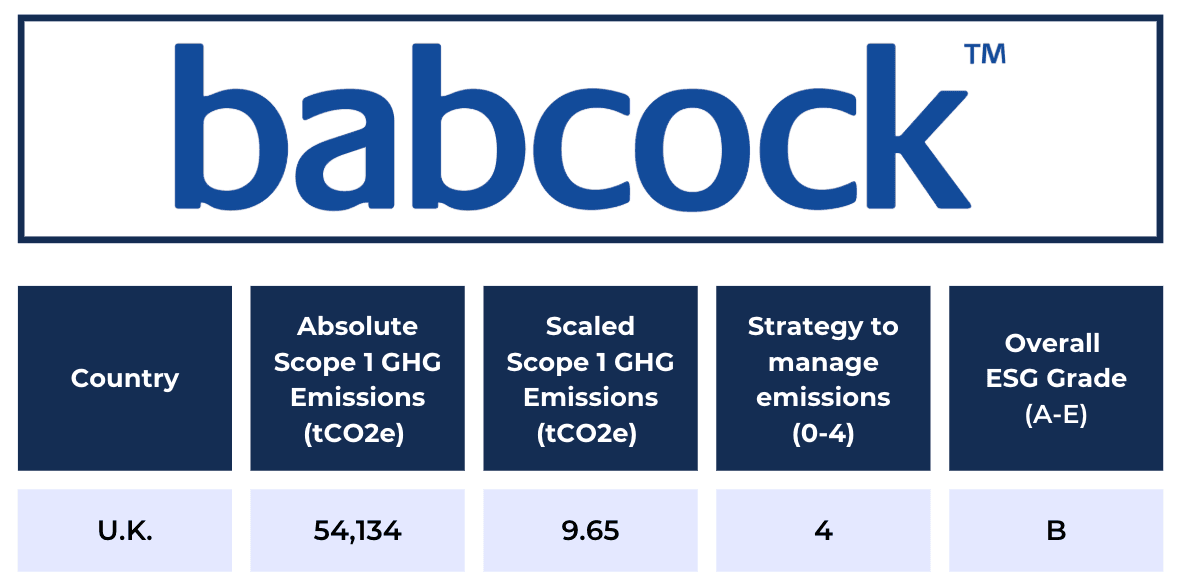

Leader - Babcock International [LSE: BAB]

Babcock International is a UK-based engineering firm with substantial marine operations, primarily focused on the construction and maintenance of naval and specialist vessels.

The company boasts a ‘Strategy to Manage Emissions’ metric score of 4 on the Integrum Platform, the highest score attainable.

The company has established science-based emissions targets for both near and long-term reductions, and actively measures Scope 1, 2, and 3 emissions across its operations.

Babcock further supports supply chain decarbonization through provision of a dedicated carbon reporting tool (JOSCAR Zero) to its suppliers.

Notably, 28% of its fleet now consists of Ultra Low Emission Vehicles (ULEVs), underscoring its commitment to sustainable mobility.

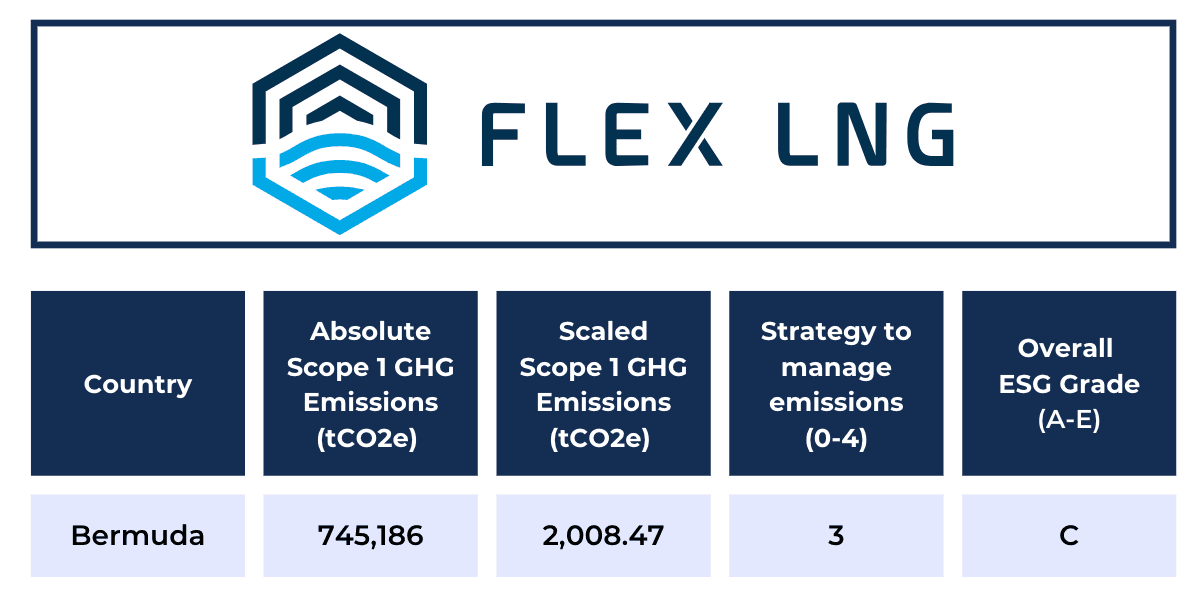

Laggard - Flex LNG [NYSE: FLNG]

Flex LNG is a Bermuda-based shipping company that owns and operates a fleet of modern liquefied natural gas (LNG) carriers.

With scaled scope 1 GHG emissions of 2,008.47 tCO2e, the company is the 6th highest direct emitter within our sample analysis.

The company's Environmental Policy outlines initiatives such as optimal use of vessels, new technologies and work on their Ship Energy Efficiency Management Plan (SEEMP).

However, this policy says nothing about the company’s use of sustainable fuel and does not include any specific quantitative emissions targets beyond regulatory obligations.

[Note: the sources used for all analysis and the methodology behind all Integrum ESG scores and grades are completely transparent - available on our website, Platform or via request.]

Impact within & beyond the shipping industry

Whilst final details on thresholds and implementation for the IMO Carbon Pricing scheme are expected to be confirmed by October 2025, rising emissions could trigger significant levies.

Firms lacking robust emissions strategies are at risk of higher costs - facing expensive reactive changes which could be avoided through strategic investments made now to improve their processes.

Moveover, the effect of this new regulation will be felt throughout the global economy, with shipping emissions relevant to the supply chains of all industries.

Companies that rely heavily on carbon-intensive shipping routes or partner with high-emission fleets may face increased operational costs, as carriers pass the price of carbon up the supply chain.

In turn, they may seek to manage this risk by opting for carriers with greener fleets, optimising route planning, or even re-shoring production to reduce long‐haul transport emissions.

Looking Ahead

Despite some criticism over ambition and enforcement, the IMO’s carbon pricing model marks an important step toward cleaner shipping and ESG integration, directly linking emissions to financial costs for the first time.

This shift is forcing companies to reconsider traditional business models, balancing the cost of emissions with efficiency and market strategy.

For investors and executives, navigating the intersection of regulation, innovation, and sustainability is now essential.

At its core, carbon pricing is elevating sustainability to a central priority for the industry and, as the sector evolves, companies that fail to adapt to this new pricing landscape risk both financial penalties and a widening gap behind forward-thinking competitors.