Shai began his career on the buyside at what is now JP Morgan AM, before moving to the sellside where he worked in several research roles. He was Head of Research at Macquarie Group for 10 years before founding Integrum ESG in 2018. Shai has an M.A. from Cambridge University.

You cannot charge the cost of ESG data to your fund… BUT you can charge the cost of ESG ratings to your fund.

Confused? Let us explain.

On Friday, the FCA published a policy statement (PS25/4) which confirms that asset managers can charge the cost of ‘investment research’ to their clients.

Practically, this means they can put some of the commissions charged by their brokers into a separate pool and use that money to pay their investment research providers at the end of the year. Many smaller asset managers already use what is called an RPA (‘Research Payment Account’) to charge the cost of investment research to the fund, as allowed under UK MiFID II.

But most firms concluded the RPA mechanism would be too challenging operationally, and were convinced that their investor clients would reward them from absorbing the cost of third-party research themselves (even though, as a % of the fund’s value, that cost was miniscule).

But the situation has changed in the past 2 years.

The FCA has finally acknowledged that the ‘unbundling’ of commission enforced by the MiFID II legislation (which still applies in the UK), saved investors very little in cost, and is probably lowering their investment returns.

As asset management companies started absorbing the cost of third-party research, they exerted huge price pressure on research providers. Some of the largest research providers soon capitulated – because they were units of investment banks that make far more profit from primary securities issuance to, or trading activity with, their asset manager clients.

Research providers launched wave upon wave of cost reductions in response to this price compression, and the FCA has had to acknowledge that the quantity and quality of investment research has fallen significantly, to the detriment of UK capital markets and investors.

So the FCA has reversed its ‘unbundling’ policy and has now finalised a ‘joint payment option’.

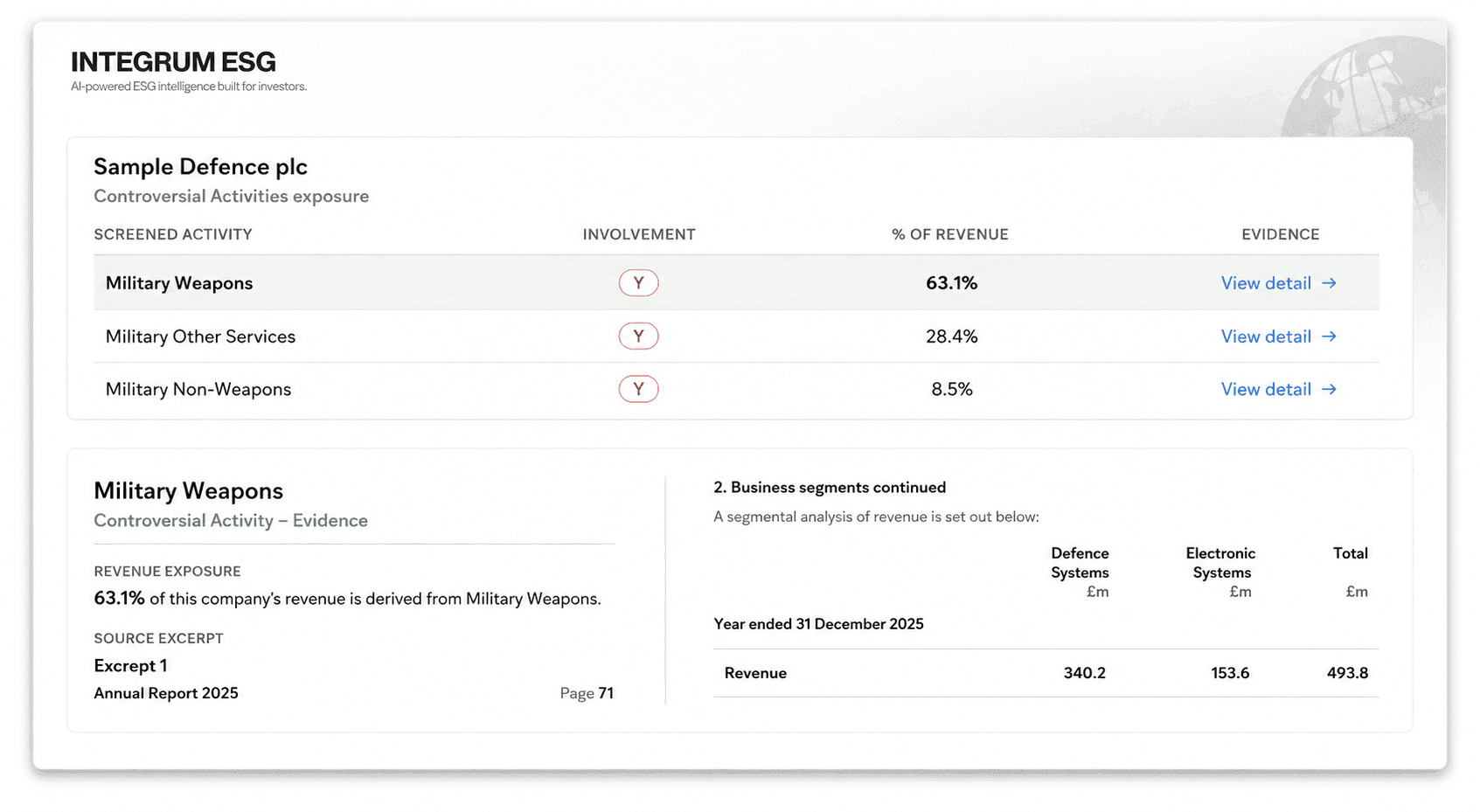

Good news for equity research teams - but will it affect providers of ESG data & analytics? 📊

To answer this, we need to consider the FCA definition of ‘investment research’, which is set out in the FCA ‘handbook’ (precisely, the Conduct of Business Sourcebook, section 12.2).

We would argue that whilst there is a trend of asset managers ignoring ESG ratings on issuer companies and seeking detailed raw ESG data instead, raw underlying data would not meet the FCA definition of investment research. But an ESG rating, underpinned by raw data, would certainly classify as “information…suggesting an investment strategy, explicitly or implicitly, concerning…the issuers of financial instruments.” (FCA COBS 12.2.1).

Why do we say ‘certainly’? 📝

Because the FCA concluded last year that ESG ratings providers must be brought within their regulatory perimeter, as “market participants become more reliant on ESG information to support their trading, investment and capital allocation decisions, and to meet their reporting requirements.”

The FCA regards ESG ratings as influencing investment decisions – thereby meeting their definition of investment research.

So fund managers – you can (and should) integrate ESG ratings into your investment research, and you can charge the cost to your funds.

But do your clients a favour – make sure the ratings are supported by timely, high-quality data, so they actually have a positive impact on your investment decision making.